In this article, US-based investment manager Direxion — and provider of the Direxion Connected Consumer ETF [CCON] and Direxion Work From Home ETF [WFH] — explores the key companies reporting fourth quarter earnings in both the work from home and connected consumer themes. Some of the companies mentioned below have already reported.

Momentum continues for the evolving workplace and consumer

Technological and societal trends are always in motion. Lately, some of the most significant changes are happening directly in our day-to-day with work and life. The workplace has changed dramatically over the years, in almost every way possible, and that was especially true in 2020. How consumers are engaging with everyday products and services has also undergone structural change. That, too, was especially prevalent in 2020.

Going forward, where and how companies operate continues to develop and evolve. Businesses have become more distributed, teams have gone global, and employees have become more agile with a greater need for everything to be on-demand. Looking back, the “work from home” expression had become synonymous with 2020, but companies and businesses are set to continue to invest in and prioritise the digitisation of the workplace.

The future of work is remote, and enterprise spend in the future reflects this paradigm. According to a recent Gartner survey on the global IT marketplace, worldwide IT spending is projected to total almost $3.8trn in 2021, a 4% increase from 2020.

IT Investment is expected to grow 4% in 2021 with enterprise software seeing the largest increase of over 7% worldwide IT spending forecast (millions of US dollars).

2019 Spending | 2019 Growth (%) | 2020 Spending | 2020 Growth (%) | 2021 Spending | 2021 Growth (%) | |

Data Center Systems | 214,911 | 1.00 | 208,292 | -3.10 | 219,086 | 5.20 |

Enterprise Software | 476,686 | 11.70 | 459,297 | -3.60 | 492,440 | 7.20 |

Devices | 711,525 | -0.30 | 616,284 | -13.40 | 640,726 | 4.00 |

IT Services | 1,040,263 | 4.80 | 992,093 | -4.60 | 1,032,912 | 4.10 |

Communications Services | 1,372,938 | -0.60 | 1,332,795 | -2.90 | 1,369,652 | 2.80 |

Overall IT | 3,816,322 | 2.40 | 3,608,761 | -5.40 | 3,754,816 | 4.00 |

Source: Gartner (October 2020). Forecasts are limited and may not be relied upon. There is no guarantee an increase in spending or investments in the IT sector will translate to favourable fund performance.

We believe these dynamics go beyond simply enabling the ability to “work from home,” but that companies and enterprises are actively becoming more digital. This is a secular shift, not a cyclical one. The core drivers behind the shift continue to be cloud technology, cyber security, online project and document management, and remote communication.

When it comes to the consumer, we continue to see new behavioural trends emerge across all areas of life. Beyond shopping and consumption, the way we learn, engage, play, and think about our health are all changing right before our eyes. New experiences and different mediums are playing a large role in meeting evolving consumer needs, and the core pillars of home entertainment, online education, remote health and well-being, and virtual and digital social interaction are set to benefit.

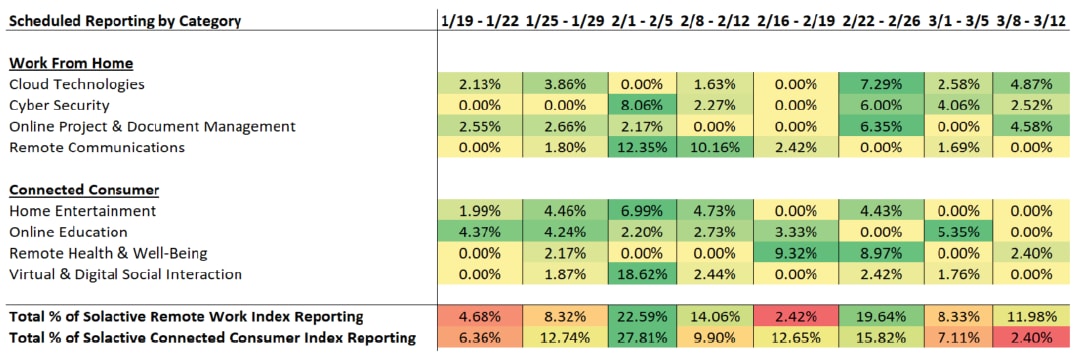

Fourth quarter earnings season is set to be an important one for many of the names within the major pillars driving change in the workplace and for the consumer. We will be looking for the numbers to match the rhetoric, and for cues around the ongoing environment. The busiest weeks for investors in regard to earnings releases will be during the first and last weeks of February.

Source: Bloomberg, as of 11 January 2021

Online project and document management: Prioritising productivity for the evolving workplace

Along with investing in a more agile, more digital workplace, businesses have been working to support to productivity, creativity, and collaboration both internally and externally. Capabilities and use cases for productivity suites and collaboration platforms are poised to expand as needs develop from a more mobile workforce and a more demanding consumer.

- Atlassian Corp [TEAM] expected 22 January: Atlassian continues to become a player to watch in the enterprise software space, especially in the software development, IT, and work management markets. With software developers and project managers in mind, the current focus for TEAM has been migrating customers over to its cloud products. With over 185,000 customers today, the management team recently noted the long runway for growth in the 800,000+ company addressable global market. Atlassian is on pace to deliver their highest marks in single quarter revenue ($471.40m) and Earning Per Share (EPS) ($0.32) in their history as a public company.

- Workday [WDAY] expected 23 February: Workday is becoming a household name for enterprise cloud applications. In other words, as demand for companies to implement longer-term digital strategies take hold, Workday’s solutions for managing human capital, finances, and products have benefited. Revenues grew 17.9% year-over-year last quarter and are expected to grow 14.2% year-over-year ($1.12bn) this quarter with an EPS of $0.56.

Source: Bloomberg, as of 11 January 2021

Remote communication: Communication digitised

Remote communication technologies and platforms are quickly becoming a standard, regardless of industry, for communication both internally and externally. This category goes beyond video communication platforms, and remote communication and the infrastructure for it is here to stay as it offers the scalability and flexibility needed for the mobile workplace and the customer that is always on the move.

- RingCentral [RNG] expected 10 February: Work together, from anywhere. RingCentral’s motto rings true for some of the core enterprise needs on the path to becoming more digital. Through their messaging, video, and phone products, mid-market and enterprise customers now account for over 50% of total revenue. Management has cited continued momentum in the accelerated adoption of UCaaS (Unified Communication as a Service), and the expected 25.5% year-over-year increase in revenues ($317.46m) is representative of that momentum.

- Twilio [TWLO] expected 5 February: The remote work revolution is fast-forwarding the demand for Communication Platforms as a Service (CPaaS), and Twilio sits at the heart of infrastructure being built to bridge the gap between voice and SMS communications and web-based applications. Twilio is becoming more likely to play a key role in the evolution of how businesses communicate with their customers via text, voice, video, and email. Revenues are expected to come in around $453.91m, a 37.0% increase year-over-year.

Source: Bloomberg, as of 11 January 2021.

Remote health and wellbeing: Health digitised

For as long as many of us can remember, medical care in both the US and around the world has looked the same today as it did 20 years ago. COVID-19, along with technological advances, has acted as a catalyst for change in the way consumers engage with traditional healthcare products and services. With increased adoption in different technologies for better equipment and better care, consumer needs and demands for healthcare products and services are changing. And like many other areas of our lives, healthcare is becoming more digital.

- Teladoc Health [TDOC] expected 26 February: The largest US telehealth company has benefitted from an acceleration in adoption trends throughout 2020, and they are expected to report top-line growth of almost 139% year-over-year ($373.68m vs. $156.49m), which represents a significant increase in revenue growth from just a year ago (+27%). While Teledoc is seemingly well on its way to capitalising on its vision of virtual primary care, we will be watching for rhetoric around further growth potential and their outlook for 2021.

- 1Life Healthcare [ONEM] expected 18 March: A newly listed name in January 2020, 1Life Healthcare (more commonly known as One Medical) is a west-coast based chain of primary healthcare clinics. Their membership-based primary care service has an integrated digital health system, allowing One Medical to deliver the benefits of easy and digital access to care and lower costs to its members. ONEM is expected to report consensus revenues of $106.91m in March with losses of $0.12 per share, which would represent significant increases from their first earnings report as a public company back in March 2020.

Source: Bloomberg, as of 11 January 2021.

Virtual and digital social interaction: Engaging with the world around us

Remote communication technologies and platforms are quickly becoming a standard, regardless of industry, for communication both internally and externally. This category goes beyond video communication platforms, and remote communication and the infrastructure for it is here to stay as it offers the scalability and flexibility needed for the mobile workplace and the customer that is always on the move.

- Snap [SNAP] expected 4 February: Snap has continued to evolve its portfolio of products and has introduced new ways for users to engage with the platform, and each other. Snap Spotlight, introduced on 23 November, has given users the opportunity to create viral videos and engage with the community. Along with the Map, Chat, Camera, Stories/Discover, and Sounds functions, Snap continues to add momentum in engagement growth which is providing valuable scale to advertisers. Snap is expected to deliver 51.5% year-over-year revenue growth ($849.70m), and we will be watching user activity as well.

- Weibo Corp [WB] expected 26 February: Weibo is a social media platform and microblogging website for people to create, distribute, and discover content. With over 523 million monthly active users (as of the third quarter 2020), Weibo has taken steps to evolve their platform and prioritise engagement and social interaction by introducing more video content and promoting live events with major media partnerships. While 2020 represented challenges around the advertisement centric revenue model, they are expected to report year-over-year revenue growth of 5.9% in February.

Source: Bloomberg, as of 11 January 2021.

The COVID-19 pandemic has not only caused major short-term impacts but has also created long-term disruption to both living and working conventions. One of the long-term trends the coronavirus has accelerated is, “what, where and how” consumers and the workforce behaves.

This article was originally published in Direxion’s Spotlight newsletter, which covers the latest news on the top investment themes.

Disclaimer Past performance is not a reliable indicator of future results.

CMC Markets is an execution-only service provider. The material (whether or not it states any opinions) is for general information purposes only, and does not take into account your personal circumstances or objectives. Nothing in this material is (or should be considered to be) financial, investment or other advice on which reliance should be placed. No opinion given in the material constitutes a recommendation by CMC Markets or the author that any particular investment, security, transaction or investment strategy is suitable for any specific person.

The material has not been prepared in accordance with legal requirements designed to promote the independence of investment research. Although we are not specifically prevented from dealing before providing this material, we do not seek to take advantage of the material prior to its dissemination.

CMC Markets does not endorse or offer opinion on the trading strategies used by the author. Their trading strategies do not guarantee any return and CMC Markets shall not be held responsible for any loss that you may incur, either directly or indirectly, arising from any investment based on any information contained herein.

*Tax treatment depends on individual circumstances and can change or may differ in a jurisdiction other than the UK.

Continue reading for FREE

- Includes free newsletter updates, unsubscribe anytime. Privacy policy