Investors focus on central banks and US data

Investors are focusing on central banks, US CPI and labour-market data on 12 June as the FTSE 100 trades higher. Middle East risks remain the main external threat, while Oracle's AI spending plans are keeping the semiconductor cycle in focus.

Chief Market Analyst

The FTSE 100 trades higher as investors watch global signals

The FTSE is trading higher on 12 June, with only a limited number of fresh market catalysts available during the session. That leaves investors looking beyond the UK benchmark itself and towards global macro signals for direction.

The lack of a clear domestic trigger does not mean the backdrop is calm. Markets are still balancing central-bank risk, US inflation signals and geopolitical uncertainty, all of which can quickly shape sentiment across UK equities even when company-specific news is limited.

Middle East risks remain the main external threat

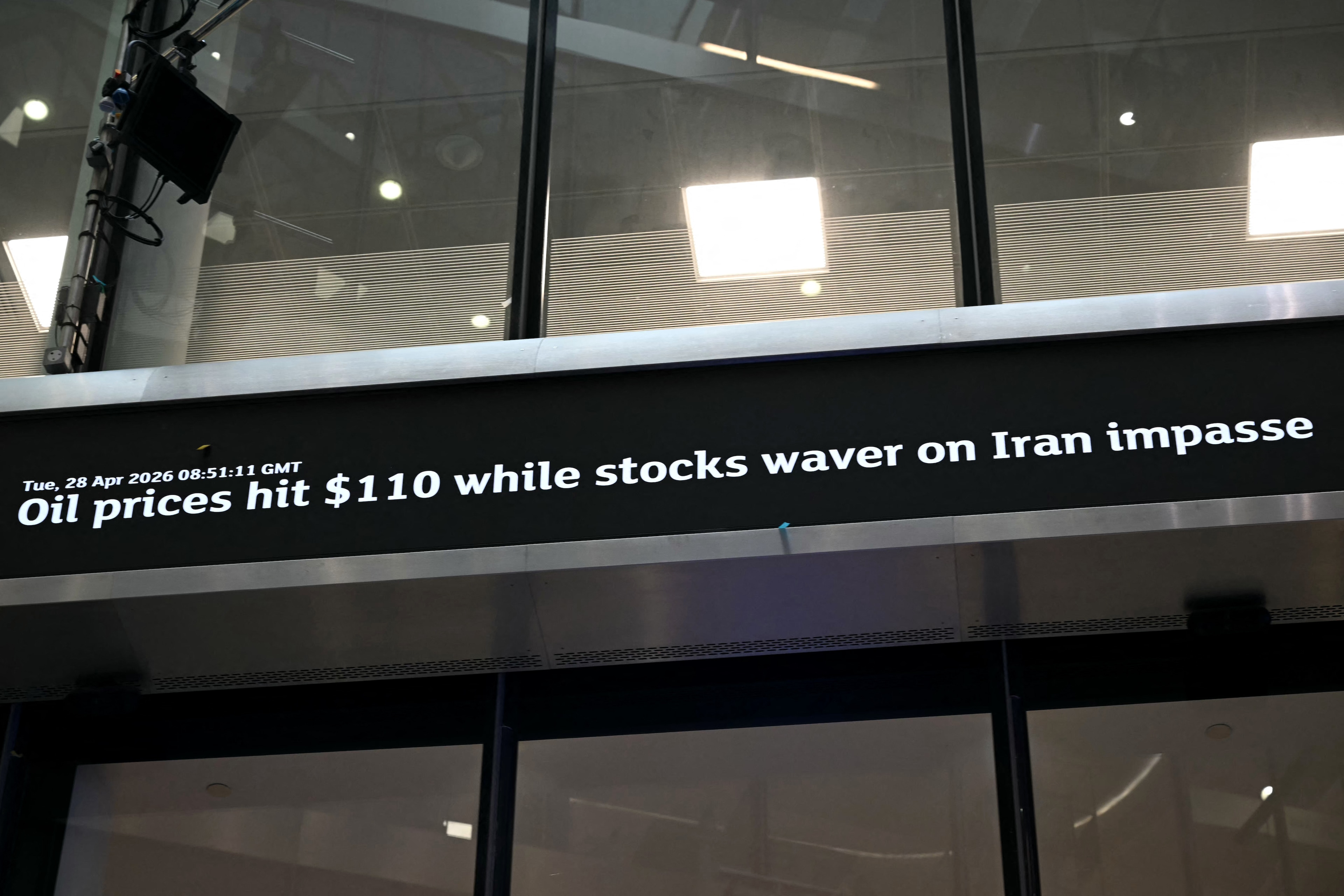

The situation in the Middle East remains complex and uncertain, and for now it continues to represent the dominant external risk factor for financial markets. Investors are still cautious about the potential effects on energy prices, shipping routes and wider risk appetite.

For the UK market, the immediate question is whether geopolitical risk stays contained enough for traders to focus on policy and data, or whether a fresh escalation forces another defensive shift. That uncertainty is one reason the index is struggling to generate much conviction at the open.

Oracle keeps the AI spending cycle in view

Oracle's latest earnings report is unlikely to have a significant direct impact on the UK benchmark index. However, the company's plans for another substantial round of AI-related investment have reinforced expectations that the semiconductor industry's current hypercycle may continue for longer than previously anticipated.

For technology stocks, that is an important signal. The AI infrastructure build-out remains one of the main themes supporting global growth and semiconductor-linked equities, even as investors question whether valuations can keep expanding if interest-rate expectations stay restrictive.

Central banks and US data remain the main policy focus

Market participants in London will keep one eye on the 12 June meeting of the European Central Bank, while focusing primarily on upcoming US CPI and labour-market releases. Those data points are expected to provide important signals for global monetary policy and could influence how investors price the next moves from major central banks.

The FTSE is therefore exposed to a broader global rates debate, not just local UK news. A stronger inflation or jobs signal from the US could keep bond yields elevated and limit risk appetite, while softer data may revive hopes that policy pressure can gradually ease.

The Bank of England decision is moving onto the radar

Attention is also gradually shifting towards next week's policy meeting of the Bank of England. Investors remain cautious as they assess the implications of persistent inflation pressure, slowing economic momentum and ongoing geopolitical risks.

For now, the market is likely to remain sensitive to any development that changes the balance between growth and inflation. The FTSE may still find support from defensive and energy-linked parts of the index, but the wider direction is likely to depend on whether central banks can sound confident without deepening concerns about the economic outlook.

FTSE 100 expected to open lower as central banks, Iran and tech valuations stay in focus

The FTSE 100 is set for a softer start as investors weigh central-bank risk, renewed tension around Iran and whether global technology valuations can still hold up. Higher oil prices are offering some support through BP and Shell, but US CPI could become the session's main driver.

The Week Ahead: US inflation, Oracle earnings, ECB rate decision

Welcome to Michael Kramer's pick of the key market events to look out for in the week beginning Monday 8 June.

ECB raises rates as Eurozone stagflation risk deepens

The ECB has delivered a 25-basis-point rate rise, but the move lands in an uncomfortable mix of weaker growth and higher inflation projections. With energy costs still driving the shock, the euro and European equities may remain sensitive to every hint on the next rate move.