As part of a new series showcasing insights from top financial experts, this article was contributed by financial strategist and founder of Weipedia, Wong Kon How.

Beside Inflation, Bonds are a Concern

US June CPI was the lowest at 3%, down from its high of 9% in June 2022. The next day, JP Morgan’s Jamie Dimon warned that inflation and interest rates might stay higher. Additionally, Fed Chairman Jerome Powell emphasised that the central bank is looking for “greater confidence” that inflation will return to the 2%, as stated in most of the meetings over the past months and on 15 July, despite the declining CPI.

DECODING JAMIE DIMON

Dimon said in a statement along with the bank’s second-quarter results: “There has been some progress bringing inflation down, but there are still multiple inflationary forces in front of us: large fiscal deficits, infrastructure needs, restructuring of trade and remilitarization of the world,” “Therefore, inflation and interest rates may stay higher than the market expects.”

Part of the fiscal, infrastructure, trade, and military spending requires budgets from bond sales. However, US, UK, and EU bonds are trading much lower than their peak in March 2022. There is a risk that bonds may continue to trend lower, leading to higher yields and interest rates.

Source: TradingView

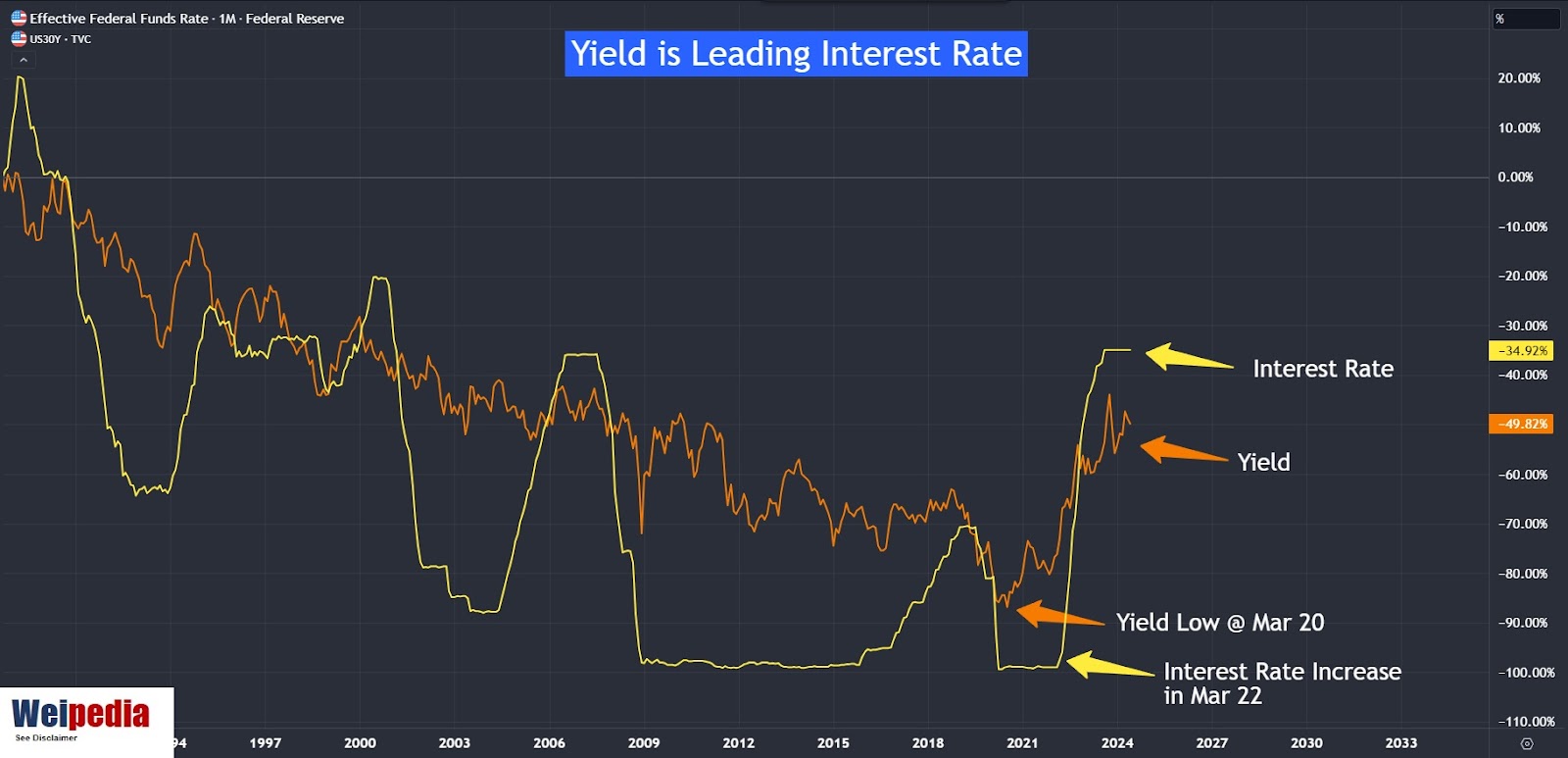

RELATIONSHIP BETWEEN BONDS, YIELD AND INTEREST RATES

When government bonds are down, yields will be higher. Since yields and interest rates move in tandem, this will cause interest rates, including the Fed funds rate, to trend higher. From the illustration above, since the bonds peaked in March 2020, yields bottomed in the same month. The bonds have been trending lower since then, and the yields and interest rates have been trending higher.

Below illustrate yield taking its lead moving higher followed-by two years later the Fed Fund rate having its first hike in March 2022. During this period, the yield curve started its inversion in June 2022.

With the ongoing money printing and trade deficits in the US and UK, the natural outcome is inflation. A lowering of bond prices may worsen the situation.

Source: TradingView

EXAMINE INTEREST RATES THROUGH THE LENS OF BONDS

In addition to inflation numbers influencing interest rates, bond analysis is also crucial. What is your outlook on bond prices in the coming months?

With bonds trading much lower, it indicates that investors are losing confidence in the country’s ability to generate future economic growth. Continuous borrowing raises concerns among investors about the worst-case scenario: the ability to fulfil the principal sum at the end of the tenure. The recent shocking election results in the UK and France, along with a divided US Congress, suggest that the outlook for these bonds may not be favourable.

MARKET OUTLOOK

Therefore, bonds should still be under pressure, yield and interest rates should remain higher with a short-term easing, and stock markets should begin to get more volatile for the rest of the year. Below was shared last month with Nasdaq targeting at around 21,000, and it reached this target on 11 July. With more volatility in US stocks, I am expecting more trading opportunity ahead.

Source: TradingView

Source: TradingView

This article was contributed by:

This document does not constitute an offer or solicitation to buy or sell any investment product(s). It does not take into account the specific investment objectives, financial situation or particular needs of any person. Investors should seek advice from a financial adviser before investing in any investment products or adopting any investment strategies. In the event that the investor chooses not to seek advice from a financial adviser, he/she should consider whether the product in question is suitable for him/her. The investment product(s) discussed herein are subject to significant investment risks, including the possible loss of the principal amount invested. Any examples provided are for illustrative purposes only. Past performance of investment products is not necessarily a guide to future performance. Weipedia and its affiliates may deal in investment products in the usual course of their business, and may at any given time be on the opposite side of trades by investors and market participants. Any statements or information expressed by other organisations are of the respective authors. Weipedia and its affiliates make no warranty as to the accuracy, completeness, merchantability or fitness for any purpose, of the information contained in this document or as to the results obtained by any person from the use of any information or investment product(s) mentioned in this document. Weipedia undertakes no responsibility to update this document. Weipedia reserves the right to make changes to this document from time to time. In no event shall this document, its contents, or any change, omission or error in this document form the basis for any claim, demand or cause of action against Weipedia and/or any of its affiliates and Weipedia and/or its affiliates expressly disclaim liability for the same. This document is being made available to only certain qualified recipients. In the event that this document or any part thereof is recirculated, transmitted or otherwise distributed in any format to any other person by a recipient, such recipient will have the full responsibility to ensure that such recirculation, transmission or distribution complies with all applicable laws, rules, regulations and directives in all the relevant jurisdictions. Weipedia and its affiliates hereby disclaim all responsibility and liability arising in connection with such recirculation, transmission or distribution.