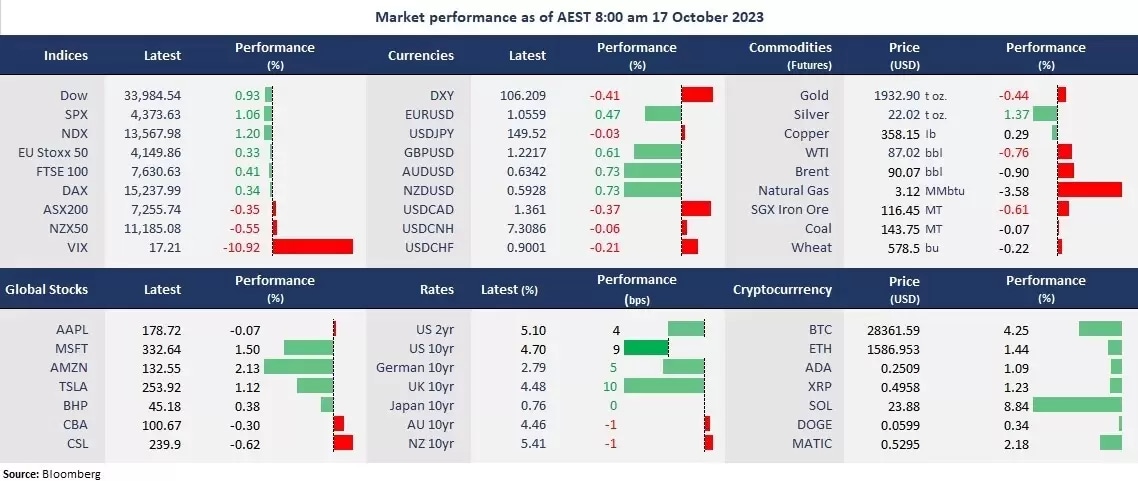

Wall Street finished higher to kick off the week on a broad-based rally as investors may have shifted focus to the upcoming major tech companies’ quarterly earnings reports from the ongoing Hamas-Israel conflicts. Mega-cap tech shares led the market gains ahead of Netflix and Tesla’s earnings later this week, while haven assets, such as gold and bonds, slipped amid the broad reversal moves after Friday’s surge, and the CBOE Volatility Index, slumped 11% to 17.2. Oil prices also pulled back as traders reassessed the Middle East turmoil, given no further escalation on the military front.

The US government bond yields climbed, but the US dollar weakened against most other major currencies due to risk appetite recovered following the equity rally. However, the restored momentum in Treasury yields remains an alert for risk assets, which could lift the USD again.

Equities across the APAC region finished lower due to risk-off sentiment on Monday. Futures point to a higher open. The Nikkei 225 futures rose 1.05%, the ASX 200 futures climbed 0.67%, and Hang Seng Index futures were up 1.17%. New Zealand is set to report the third-quarter CPI data following the national election. Consensus calls for a 5.9% year-on-year increase, slightly lower than 6% in the second quarter. The RBA meeting minutes will also be focused.

Price movers:

- All 11 sectors in the S&P 500 finished higher, with Consumer Discretionary and Communication Services, leading gains, up 1.65% and 1.47%, respectively. Energy was the laggard, up 0.66%, due to a slide in oil prices.

- Apple’s shares slumped 1% before paring losses amid news that sales of the iPhone 15 fell 4.5% compared with the iPhone 14 in the first 17 days after release in China. Apple faces challenges of fierce competition from local rivals and weakened consumer demand.

- Pfizer’s shares jumped 3.5% despite the drug maker slashing US$0 billion sales guidance for 2023. Pfizer cut sales of Paxlovid antiviral to US$1 billion from $8 billion and lowered forecasts of Covid shots by US$2 billion to US$11.5 billion for 2023 amid weakened demands.

- Bitcoin spiked to above 30,000 before cutting gains as BlackRock denied rumours that the SEC approved its Bitcoin ETF application. The largest fund manager confirmed that the ETF application “is still under review.” Despite the retreat, Bitcoin is still in strong upside momentum, up 4.5% in the 24 hours to about 28,500 at a two-month high.

- Crude oil slipped, with the Brent futures pulling back to under US$90 per barrel as fears of an escalation in the Hamas-Israel war faded somewhat. However, oil prices may continue to face the upside pressure with the ongoing geopolitical tensions.

ASX and NZX announcements/news:

- Synlait Milk (ASX: SM1, NZX: SML) will enter into an arbitration process with A2 Milk to determine the validity of the notice of cancellation of the exclusive agreement as a supplier.

Today’s agenda:

- New Zealand’s Q3 CPI

- RBA Meeting Minutes

- Canada’s September CPI

Disclaimer: CMC Markets is an order execution-only service. The material (whether or not it states any opinions) is for general information purposes only, and does not take into account your personal circumstances or objectives. Nothing in this material is (or should be considered to be) financial, investment or other advice on which reliance should be placed. No opinion given in the material constitutes a recommendation by CMC Markets or the author that any particular investment, security, transaction or investment strategy is suitable for any specific person. The material has not been prepared in accordance with legal requirements designed to promote the independence of investment research. Although we are not specifically prevented from dealing before providing this material, we do not seek to take advantage of the material prior to its dissemination.