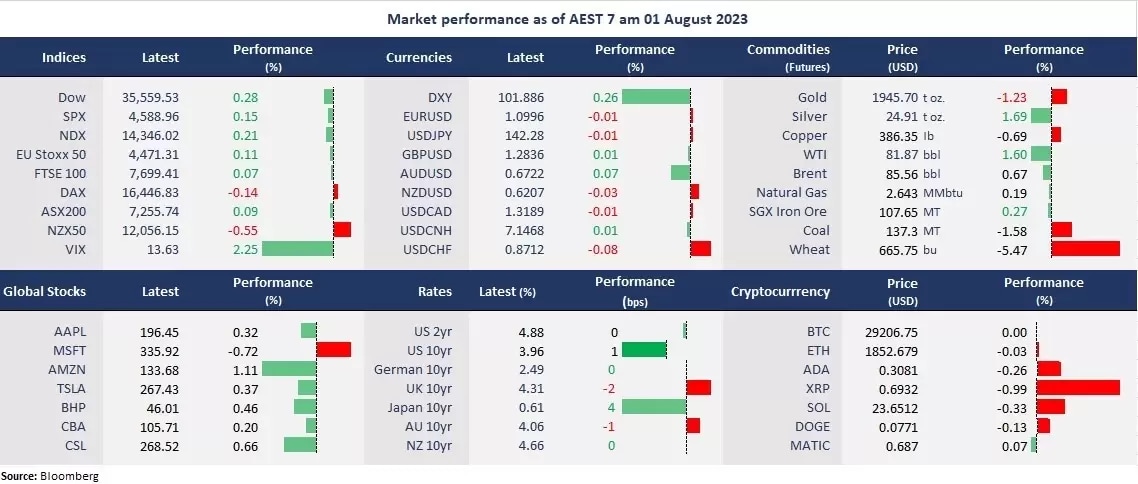

Wall Street finished slightly higher to kick off the week and booked for monthly gains. Both S&P 500 and the Nasdaq rose for the fifth month in a row as the tech-powered rally rolled into the second half of the year. Dow posted a back to back monthly gains, led by energy and financial stocks, due to the sector rotation in July. However, skepticism arises about the multi-month rally as major company earnings show a growth slowdown, while the markets may have been overbought. Apple and Amazon’s earnings reports can be the most influential events to steer broad sentiment later this week. The US non-farm payroll for July also will be the key gauge of the country’s economic health.

The US bond yields were flat but stayed at high levels after the BOJ’s policy tweak last week. The US dollar strengthened against the Japanese Yen to a 3-week high of above 142. However, the king dollar weakened against commodity currencies after China reported better-than-expected manufacturing PMI. Commodity prices were also boosted by China’s stimulus hope as officials signal to implement measures to boost consumption and the property sector. Crude oil prices extended gains to the highest levels since April 2023.

Asian markets are set to open higher ahead of the RBA’s rate decision today. The ASX 200 futures were up 0.30%, Hang Seng Index futures rose 72%, and Nikkei 225 futures climbed 0.06%.

Price movers:

- 8 out of 11 sectors finished higher in the S&P 500, with Consumer Discretionary and Materials, leading gains, up 0.56% and 0.52%, respectively. Consumer Staples and Healthcare were the laggards, down 0.46% and 0.79%, respectively. Communication services also ended in the red due to a slide in Meta’s shares.

- Apple will launch its new series of products, including the iPhone 15, featuring a few major changes in the third quarter. The new iPhone is reported to be compatible with USB-C charging and feature titanium edges instead of stainless steel.

- Rio Tinto agreed to buy 58% of a Chilean mining project from Pan American Silver Corp. Chile’s state-owned copper company Codelco owns the other 42%. Rio Tinto’s shares slumped amid a disappointing half-year report last week but reversed some losses on Monday.

- Oil futures rose about posts the best monthly gain in more than one year. OPEC +’s output cuts, improved demand outlooks, China’s stimulus measures, and faded recession fears all contributed to the rally. The WTI futures may face near-term resistance of about $83 per barrel, a breakout of this level may take it to head off $90.

ASX and NZX announcements/news:

- No major announcement.

Today’s agenda:

- RBA rate decision

- US ISM manufacturing PMI & Jolts Job Openings

Maximize your potential gains! Take immediate action and seize the investment opportunities that await you. Login to the platform now!

Disclaimer: CMC Markets is an order execution-only service. The material (whether or not it states any opinions) is for general information purposes only, and does not take into account your personal circumstances or objectives. Nothing in this material is (or should be considered to be) financial, investment or other advice on which reliance should be placed. No opinion given in the material constitutes a recommendation by CMC Markets or the author that any particular investment, security, transaction or investment strategy is suitable for any specific person. The material has not been prepared in accordance with legal requirements designed to promote the independence of investment research. Although we are not specifically prevented from dealing before providing this material, we do not seek to take advantage of the material prior to its dissemination.