With the busiest part of earnings season behind us, the focus in the coming week shifts back to central bank monetary policy, with the US Federal Reserve and the Bank of England each holding rate-setting meetings this week. Although earnings season may have peaked, a few big names are still to report, including chip industry heavyweights Arm and Qualcomm, both on Wednesday. But perhaps the most significant upcoming event is Tuesday’s US presidential election – more on that below.

US election

Tuesday 5 November

The US election is likely to have a significant impact on financial markets, both in the short and long term. Traders and investors are bracing themselves for a period of volatility in what the polls suggest is an extremely close race for the White House. The truth is that nobody knows what will happen, but it seems likely that the result will be decided by voting in seven swing states, with Pennsylvania carrying the most electoral votes of the group. The tightness of the race suggests that it may take a few days for a clear winner to emerge.

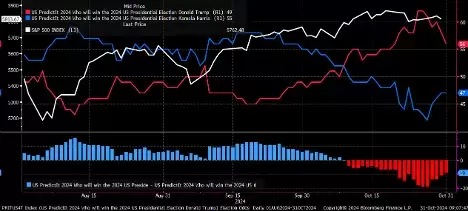

With just a few days left until voters head to the polls, former president Donald Trump’s lead over vice-president Kamala Harris in the betting market has narrowed. The US betting site PredictIt gives Trump a 56% chance of winning, down from 58% last week, with Harris on 47%, up from 44% last week. (Put another way, among those betting on Trump 56% back him to win and 44% bet he’ll lose. Among those betting on Harris, 47% back her to win and 53% bet she’ll lose). As we commented last week, it’s important to take the betting market data with a pinch of salt. It’s possible that a small number of large stakes skewed the data in Trump’s favour, perhaps in a bid to shape voter perceptions of the two main candidates. It’s also possible that Trump supporters may be more likely to place bets than Harris supporters.

Wall Street’s benchmark share index the S&P 500, represented by the white line on the below chart, has been essentially flat since mid-August, suggesting that traders are adopting a wait-and-see approach ahead of the election.

Trump remains ahead of Harris in the US betting market